|

| Gold V.1.3.1 signal Telegram Channel (English) |

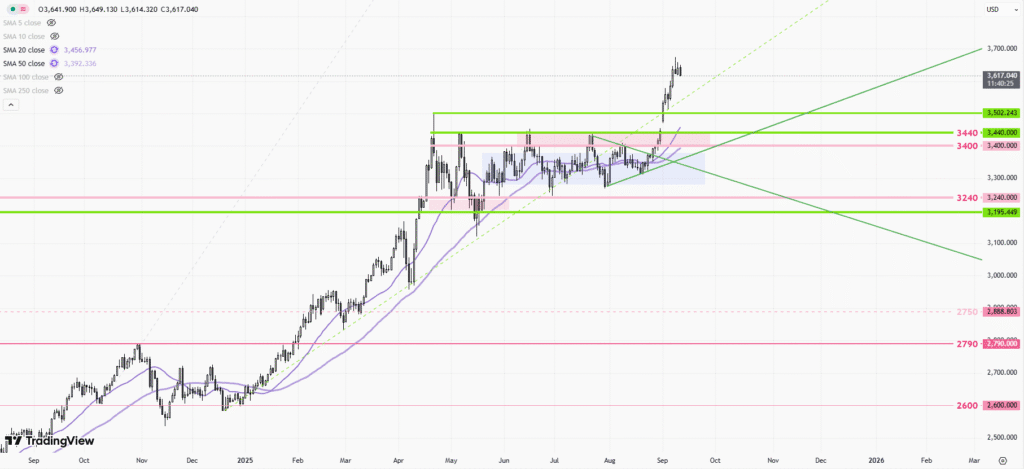

S&P 500 and Nasdaq Reach Record Highs Amid Fed Rate Cut Speculation and Key Earnings Reports

2025-08-14 @ 15:00

Stock Market Update: S&P 500 and Nasdaq Close at Record Highs Amid Rate Cut Speculation

The market landscape remains dynamic as both the S&P 500 and Nasdaq Composite closed at record highs on August 13, 2025. This surge was fueled by ongoing enthusiasm around potential Federal Reserve rate cuts and anticipation ahead of key inflation data. Investors watched anxiously as futures traded largely flat, waiting for the Producer Price Index (PPI) release that could provide fresh insight into inflation trends and monetary policy direction.

Investor Sentiment and Rate Cut Hopes

Optimism continues to drive equity prices, with many investors betting that the Federal Reserve is nearing a pivotal moment for interest rates. Recent data has reflected a slowing labor market and moderated consumer price growth, both factors that often precede a shift toward more accommodative monetary policy. The possibility of multiple rate cuts in the coming months has become a central narrative in market commentary, with analysts pointing out that even subtle inflation pressures could reinforce the argument for easing.

Despite the broader bullish sentiment, some caution is emerging. Concerns about stagflation—where the economy experiences stagnant growth alongside persistent inflation—are underlining the risks of aggressive rate reductions. If inflation remains sticky while growth falters, the Fed could find itself in a difficult position, forced to balance price stability against the need for economic stimulus.

Earnings Reports: Key Companies in Focus

Corporate earnings continue to play a crucial role in market movements. On Thursday, several major companies are slated to report results, including John Deere, Tapestry, and Applied Materials. Applied Materials, in particular, is expected to post strong third-quarter sales, driven by robust demand for its semiconductor manufacturing equipment and stabilizing performance in China. This reflects a broader trend in the chip industry, where supply chains are recovering and global demand remains resilient.

John Deere and Tapestry will also draw investor attention, as their results may provide deeper insight into the strength of industrial and consumer segments. The performance of these companies could offer important clues about the health of sectors such as machinery, agriculture, and discretionary retail.

Inflation Data: All Eyes on the PPI

The upcoming Producer Price Index release is a key focal point for both economists and market participants. PPI tracks the average change in selling prices received by domestic producers for their output, offering an early reading on inflationary pressures throughout the economy. A higher-than-expected PPI print would signal rising costs at the wholesale level, potentially foreshadowing increased consumer prices in the future.

Traders and policymakers will dissect the data to assess whether inflation is truly easing or if underlying pressures remain. This assessment is vital for shaping expectations around the Fed’s next move, as persistent inflation often forces central banks to maintain higher interest rates for longer.

Challenges and Risks Ahead

While record highs in major indexes are cause for celebration among many investors, risks persist beneath the surface. Volatility can increase quickly if inflation surprises to the upside or if economic growth disappoints. Additionally, geopolitical tensions, supply chain disruptions, and changes in energy prices remain wildcards that could upend expectations.

The specter of stagflation deserves particular attention. In an environment where inflation remains above target but growth stalls, traditional policy tools may become less effective. Such a scenario could challenge the prevailing optimism and force investors to reevaluate their strategies.

Sector Highlights: Technology and Industrials Lead the Way

Technology stocks have been a principal driver behind the latest rally, with investors flocking to companies benefiting from megatrends such as artificial intelligence, cloud computing, and semiconductor innovation. Stabilizing demand from China is adding extra momentum, particularly for manufacturers of advanced chip equipment like Applied Materials.

Industrials are also in focus, driven by expectations of increased infrastructure spending and a rebound in capital investments. Companies in machinery, manufacturing, and materials sectors may offer new opportunities as global supply chains recover and governments commit to modernization.

What to Watch Going Forward

The next few days are set to be critical for market direction. Key data releases, including PPI and upcoming earnings reports, will provide more context for investors. The Federal Reserve’s commentary and future meeting minutes will be closely scrutinized for clues about the timing and magnitude of any rate cuts.

For those navigating the current environment, diversification and vigilance remain crucial. Staying informed about macroeconomic developments and individual company performance can help manage risk and capitalize on emerging opportunities.

As always, the interplay between economic fundamentals, corporate earnings, and central bank policy will shape the market narrative. Whether the recent record highs mark the beginning of a longer rally or merely a temporary crest amid gathering challenges will depend on how these variables evolve in the weeks ahead.