|

| Gold V.1.3.1 signal Telegram Channel (English) |

Why Fed Rate Cuts Don’t Always Lower Mortgage Rates: What Homebuyers Need to Know

2025-08-16 @ 21:00

The Federal Reserve is widely expected to cut interest rates soon, in response to signs of a slowing labor market and softer inflation data. As a financial blogger, you might expect that when the Fed cuts rates, mortgage rates will immediately fall too. However, history—and current market conditions—suggest that the relationship is far more complex. If you’re planning to buy a home or refinance, it’s crucial to understand why mortgage rates may not drop in lockstep with Fed moves.

What Drives Fed Actions—and Mortgage Rates

When the Federal Reserve talks about cutting rates, it refers to the federal funds rate, which is the overnight interest rate banks charge each other for short-term loans. The Fed uses this tool to steer the economy, making borrowing cheaper in sluggish periods and more expensive when inflation is high. While a lower federal funds rate sets the tone for interest rates across the economy, mortgage rates are tied less directly than many consumers believe.

Mortgage rates are heavily influenced by the yields on longer-term U.S. Treasury bonds, especially the 10-year Treasury note. These yields reflect investor expectations about inflation, economic growth, and future Fed policy—all factors that extend far beyond a single rate cut. This means mortgage rates can move ahead of, or even against, Fed decisions, and often do.

Recent Rate Cut Expectations—And What They Might Mean

Currently, investors and economists are betting the Fed will announce a quarter-point rate cut at its next meeting. Predictions are being driven by a slowdown in hiring and some weaker economic indicators. But there’s also an awareness that cutting rates aggressively could stoke inflation again. The Fed must balance these risks, and its decisions remain contingent on new data.

Despite this, mortgage rates have not dropped significantly in recent weeks. In fact, the spread between the federal funds rate and average mortgage rates is wider than usual. Why? Investors are nervous about the broader economic outlook, global developments, and even the Fed’s own signaling about the path of future rates. Sometimes, mortgage rates move higher in anticipation of inflation, or stay sticky if markets feel uncertain about where things are headed next.

Why Mortgage Rates Don’t Always Follow the Fed

There are several reasons why mortgage rates may not react immediately—or even at all—to Fed rate cuts:

- Bond Market Anticipation: Mortgage rates often move based on expectations, not action. If investors already anticipate a Fed cut, mortgage rates may have already adjusted—sometimes weeks before the central bank actually decides.

- Inflation Risk: If the Fed’s rate cut is seen as likely to boost inflation, investors may demand higher yields for longer-term bonds, which drives mortgage rates up, not down.

- Economic Uncertainty: Factors such as global tensions, fluctuating oil prices, or concerns about the domestic job market can stoke volatility in bond markets, keeping mortgage rates stubbornly high.

- Credit Risk and Lender Margins: Mortgage rates also include a risk premium and lender margins that don’t fluctuate as fast as overnight rates.

Long-Term Perspective for Homebuyers and Investors

For homebuyers and those looking to refinance, the key takeaway is simple: don’t assume a Fed rate cut guarantees a significant drop in mortgage rates. The dynamic is more nuanced, shaped by a host of economic forces and market psychology. Fixed-rate mortgages, for example, reflect not only short-term Fed policy but also market forecasts for inflation over decades.

If you’re shopping for a mortgage, keep an eye on Treasury yields, economic data, and Fed communications—these factors often foreshadow changes in loan rates. Be prepared for some volatility, and consider locking in rates when market conditions are in your favor. Some buyers may prefer not to try timing the market, instead focusing on their financial readiness and the long-term nature of home ownership.

What to Watch For Next

Looking forward, several factors will determine whether mortgage rates trend downward:

- The pace and magnitude of Fed rate cuts through 2025 and into early 2026

- Continued signals from labor market data and inflation readings

- Movements in the global economy and geopolitical landscape

- Investor sentiment toward risk, especially in the bond market

It’s possible that mortgage rates will drift lower if economic conditions soften further, but this is far from guaranteed. Even seasoned experts note that mortgage rates can be unpredictable, and the best course is to stay informed and flexible.

Final Thoughts

In conclusion, while the Federal Reserve’s next steps on interest rates matter, mortgage rates march to the beat of a more complicated drummer. Rather than expecting automatic savings, homebuyers should rely on a holistic view of the market—and their personal goals—to make informed borrowing decisions.

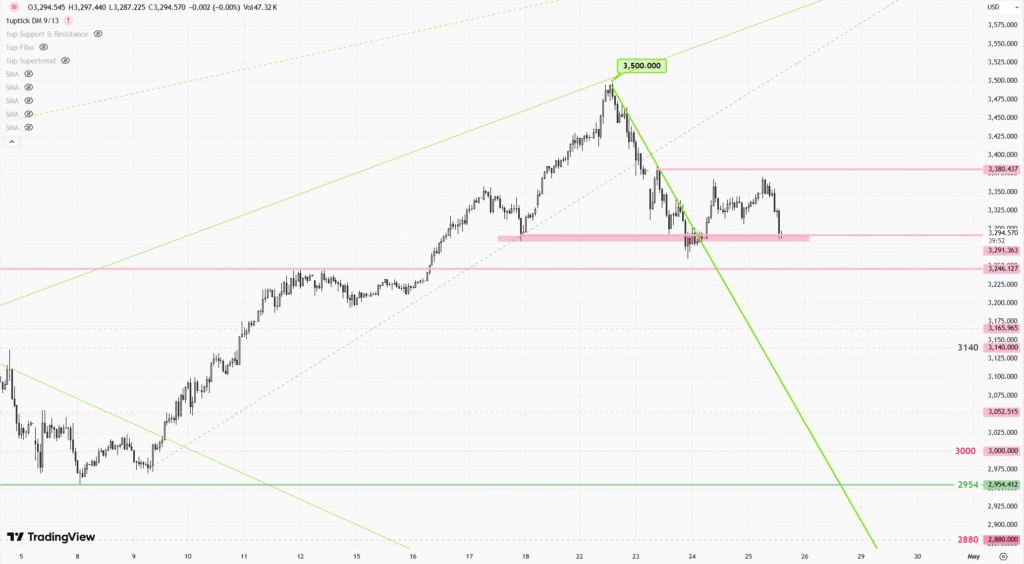

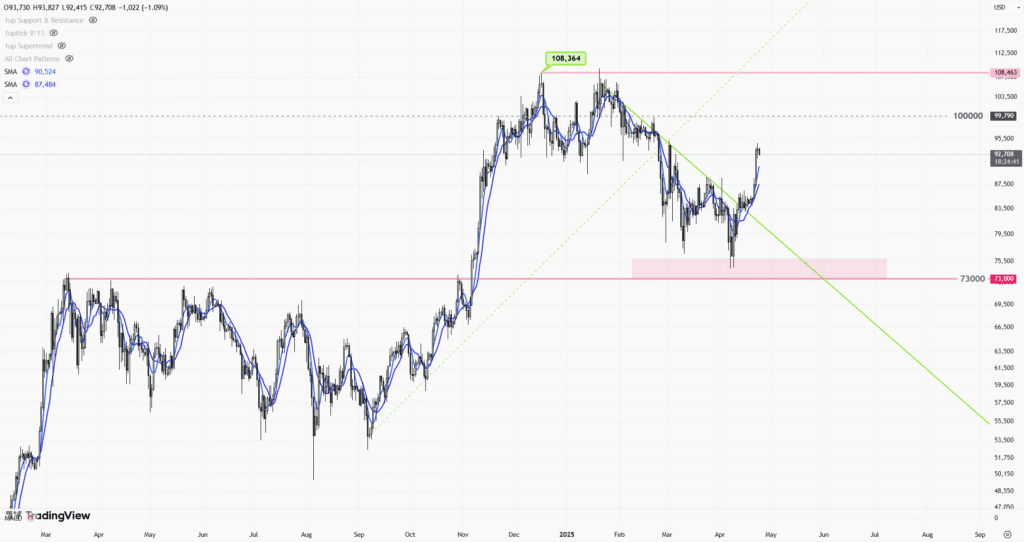

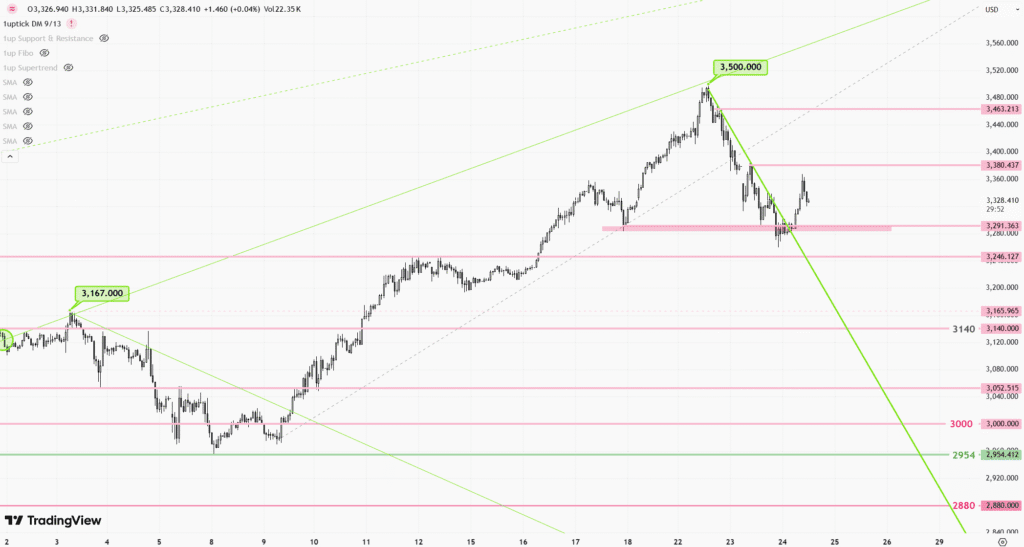

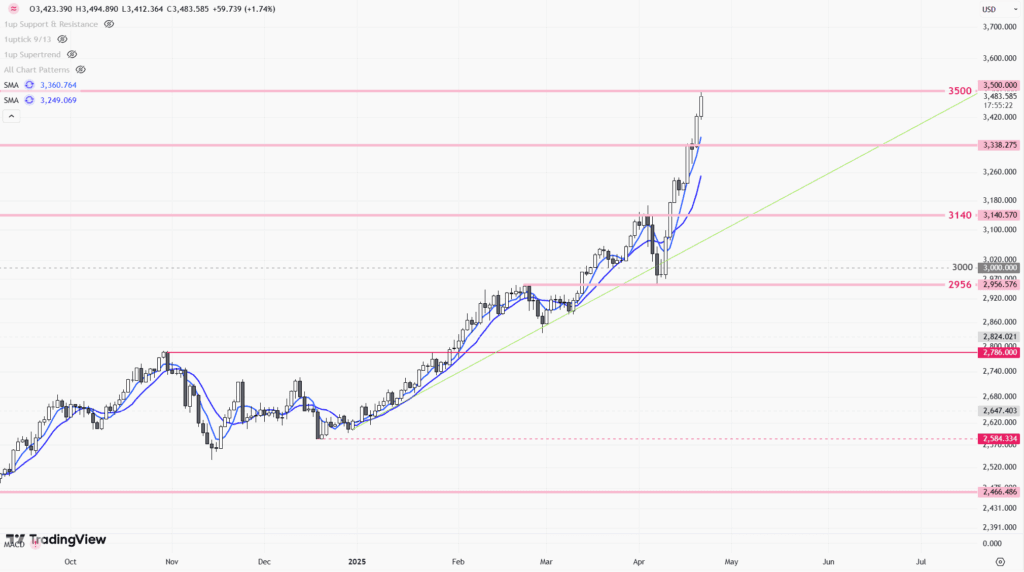

Latest Technical Analysis