|

| Gold V.1.3.1 signal Telegram Channel (English) |

U.S. Economy Surges 3.8% in Q2 2025: What This Means for Growth, Investment, and Risks

2025-09-26 @ 00:00

The U.S. economy delivered a stronger-than-expected performance in the second quarter of 2025, posting robust growth after a period of contraction. According to the latest government data, real gross domestic product (GDP) expanded at an annualized rate of 3.8% between April and June, marking the fastest pace seen since the third quarter of 2023. This substantial rebound followed a 0.5% contraction in the first quarter, bringing the first half of 2025’s annualized GDP growth to approximately 1.65%.

Key drivers of Q2 growth

The second quarter’s impressive growth was buoyed significantly by a sharp decline in imports. Imports are subtracted in the calculation of GDP, so a notable drop contributed positively to the topline figure. Earlier in the year, businesses and consumers had rushed to stockpile goods in anticipation of tariff-related price increases, resulting in a surge of imports and a drag on Q1 growth. By Q2, this effect reversed, supporting the GDP rebound.

Consumer spending also strengthened, up 1.6% compared to just 0.5% in Q1. Goods spending led the way, with services showing more modest gains. The growth in personal consumption provided a crucial pillar to the economy, even as the overall demand environment remains softer than the headline GDP number might suggest.

Private investment saw upward revision as well, with notable increases in intellectual property investment offsetting weaker results in residential and nonresidential structures. Although fixed investment growth slowed compared to earlier quarters, investment in key technology sectors remains resilient, supported in part by ongoing adoption of artificial intelligence across industries.

Government spending’s impact was relatively muted, with a slight downturn in Q2 after rebounding from declines seen earlier in the year. Meanwhile, exports slipped by 1.8%, the largest drop since Q2 2023, acting as a slight headwind.

Behind the numbers: Tariff effects and underlying risks

Despite the impressive headline figure, many analysts consider the Q2 surge more statistical than sustainable. Much of the growth was the result of the sharp reversal in import behavior, rather than broad-based acceleration in private demand. Tariffs and ongoing trade frictions have distorted business purchasing behavior, adding volatility to quarterly data.

Outside of technology-driven investment—especially related to artificial intelligence—the private sector showed subdued momentum. Ongoing inflation pressures, interest rates at multi-year highs, and tighter immigration restrictions are increasingly visible constraints on household spending and business investment.

Economic outlook for the remainder of 2025

Looking ahead, consensus forecasts point to slower economic growth as these headwinds gather force. Many expect real GDP growth to cool to just 1.5% by year-end, with conditions approaching what economists call “stall-speed dynamics.” The risk of recession remains elevated, with some forecasters assigning a 40% probability to a downturn over the next twelve months.

Policy uncertainty is also playing a significant role. Recent signals from the Federal Reserve suggest a shift towards more accommodative monetary policy in an effort to cushion the economy against slowing growth. A rate cut is broadly expected at the next Fed meeting, with additional easing likely if economic and labor market conditions deteriorate further.

What does this mean for investors and businesses?

While the headline GDP figures for Q2 are encouraging, beneath the surface the economy faces several challenges. Businesses should remain cautious in their outlooks, monitoring the impacts of tariffs, inflation, and policy shifts closely. For investors, attention will increasingly turn to sectors driven by structural factors—such as technology and intellectual property—rather than cyclical rebounds driven by trade adjustments.

Households may experience continued uncertainty around employment and income prospects, with higher borrowing costs and persistent price pressures limiting discretionary spending. Real estate markets could remain under strain, given softening residential investment and elevated rates.

In summary, the U.S. economic recovery in Q2 2025 marks a notable turnaround from Q1’s contraction, but the underlying picture is more nuanced. The rebound was buoyed by unique factors unlikely to be repeated, and the coming months could see slower growth as structural headwinds take hold. This environment calls for vigilance and adaptability from both investors and businesses as the U.S. navigates an increasingly complex economic landscape.

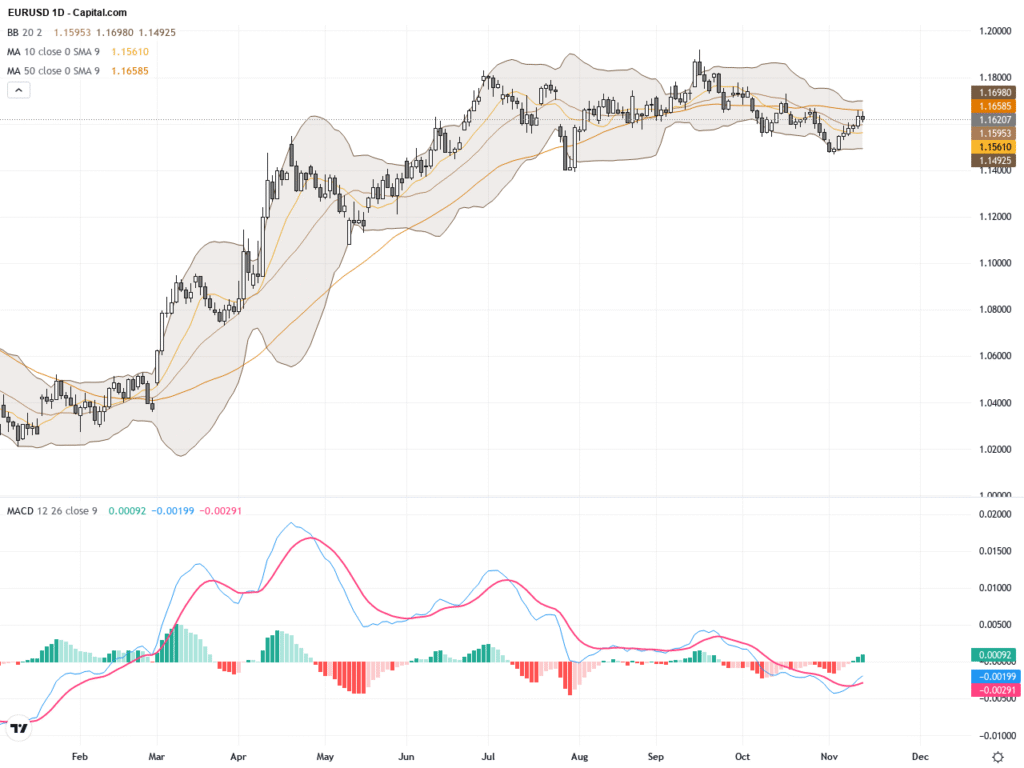

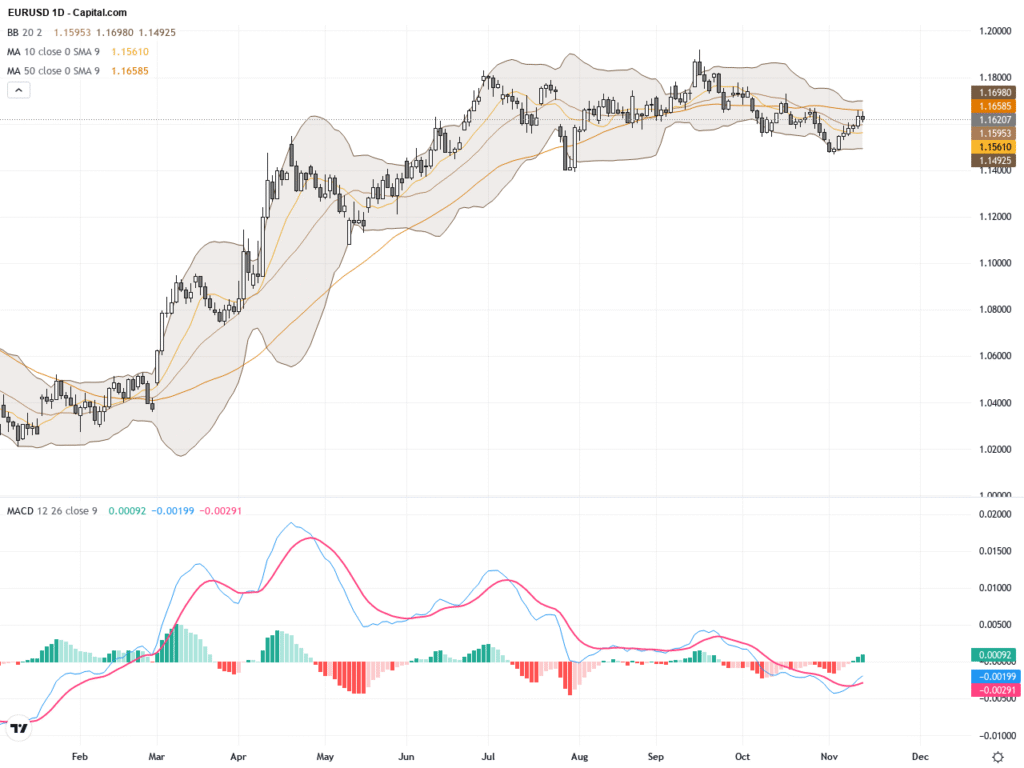

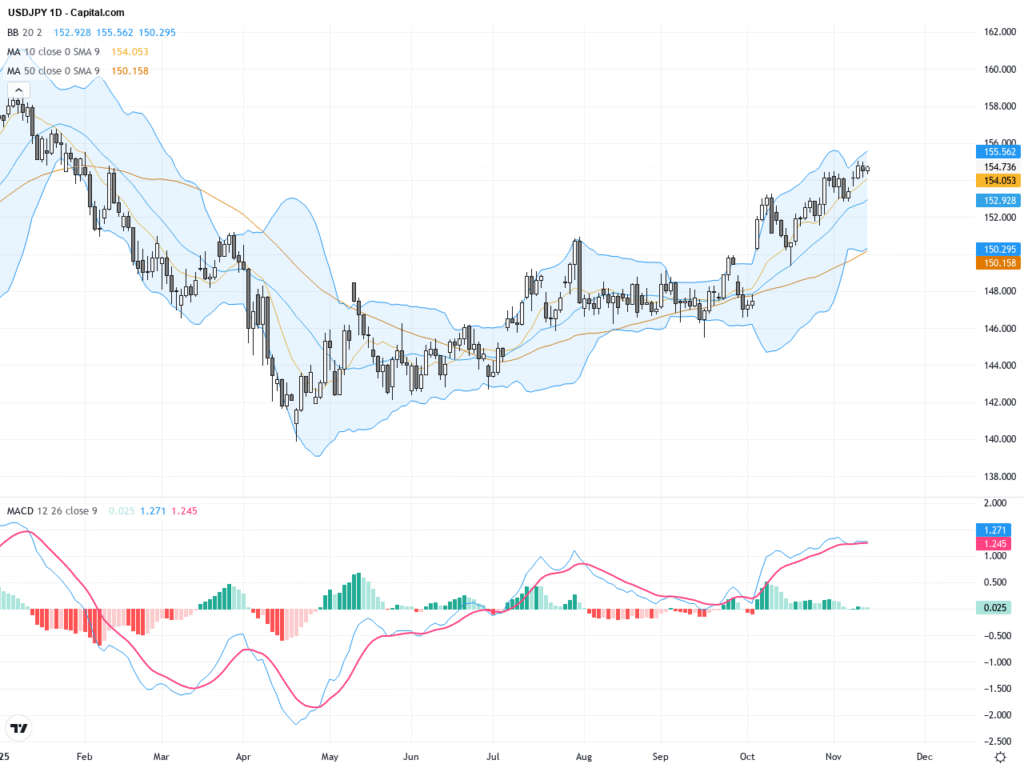

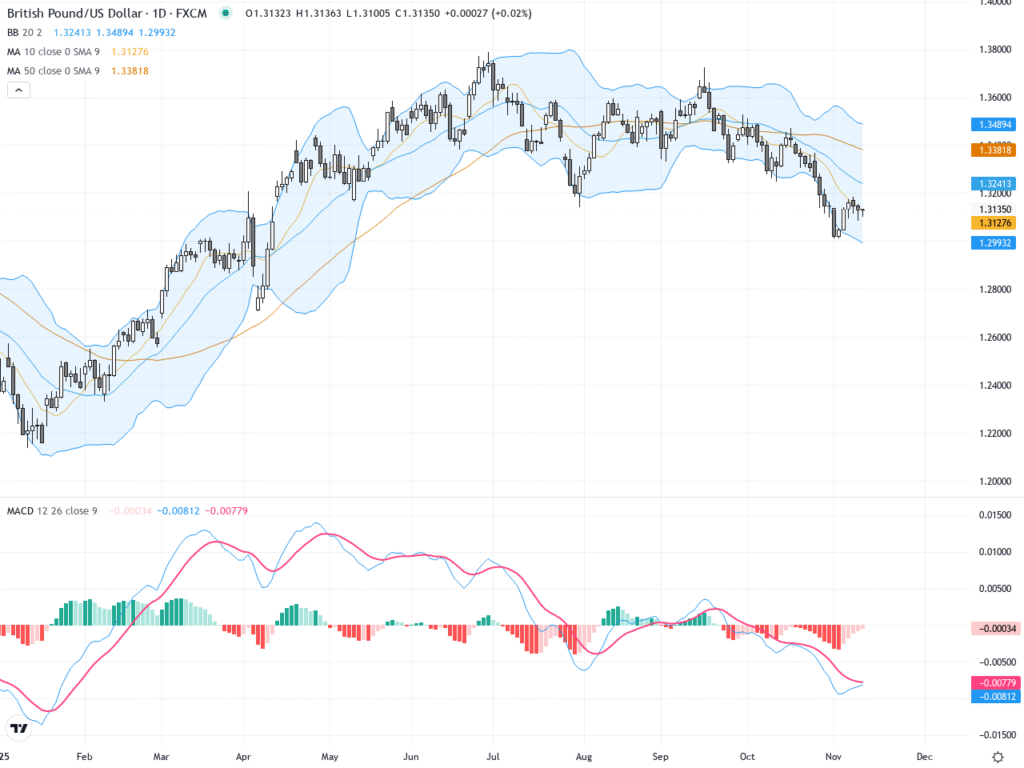

Latest Technical Analysis