|

| Gold V.1.3.1 signal Telegram Channel (English) |

European Markets Rally as Healthcare Stocks Surge Amid U.S. Shutdown Uncertainty and Mixed Sector Performance

2025-10-01 @ 20:00

European markets opened the fourth quarter with renewed optimism, overcoming a soft start and lingering external uncertainties, most notably concerns tied to the ongoing U.S. government shutdown. While broader market sentiment was cautious, the day was marked by a robust rally in healthcare and pharmaceutical stocks, helping lift European indices into positive territory and providing a fresh jolt of confidence to investors.

The pan-European STOXX 600 index rose around 0.4%, posting gains for a fourth consecutive session. Healthcare shares were at the forefront of this rally, surging by more than 3% and achieving what could be their most significant one-day advance in over a year. The sector’s exuberance was fueled largely by a watershed agreement between Pfizer and the U.S. government. Under this new deal, Pfizer will offer discounted prescription drugs via a federal website for U.S. patients, providing drugmakers with welcome tariff relief. The market viewed the agreement as a powerful de-risking event for multinational pharmaceutical companies at a time of high policy uncertainty.

Major pharmaceutical names including Novo Nordisk, Novartis, AstraZeneca, Roche, and Sanofi posted outsized gains. Notably, Novartis stock was further buoyed by an announcement that the U.S. FDA had approved its new oral therapy for a chronic inflammatory skin disease. For investors, these catalysts underscored the sector’s resilience and long-term growth prospects despite a backdrop of macroeconomic headwinds.

The mood, however, was not uniformly positive across all sectors or geographies. The technology sector saw a modest decline of 0.6%, while real estate slipped 0.8%. Several banking stocks also underperformed. Shares of Italy’s Unicredit and Intesa Sanpaolo, France’s BNP Paribas, and Spain’s BBVA and Sabadell all traded lower. The decline in Spanish banks followed news that a Sabadell board member had accepted BBVA’s takeover offer, highlighting ongoing consolidation pressures within the European financial sector.

Country-specific performance remained mixed. Spain’s leading index fell by 0.4%, in contrast with the FTSE 100 in the U.K., which jumped 0.7% to set an all-time high. This divergence reflects varying national factors and investor sentiment, with the FTSE’s rally underpinned by resilience in blue-chip defensives and continued foreign investment flows.

Macroeconomic data provided another layer of insight into the evolving market landscape. Eurozone inflation edged up to 2.2% in September. This was in line with most analysts’ expectations and further solidified the European Central Bank’s cautious stance regarding additional rate cuts. Elevated inflation may limit the space for more monetary policy easing in the coming months, raising the prospect of continued tightness in financial conditions. Meanwhile, the euro area’s unemployment rate improved slightly to 6.2%, and the region’s main equity benchmark, the Euro STOXX 50, gained 0.5%, extending its monthly and annual gains. Notably, the EU50 is up nearly 12% year-over-year, approaching historic highs set earlier in 2025.

Despite the day’s positive momentum, investors remained acutely aware of unresolved risks emanating from across the Atlantic. The U.S. government shutdown, which has already resulted in the suspension of critical economic indicators like the monthly jobs report, adds significant uncertainty to the global policy outlook. The lack of data complicates the U.S. Federal Reserve’s decision-making process ahead of its October meeting, with policy signals potentially distorted by incomplete information. For markets, the challenge is not simply political gridlock but also the abrupt pause in data that would typically guide monetary authorities.

Additionally, central bankers across Europe continue to deliver commentary closely watched by market participants for clues on the future path of interest rates and economic support measures. Volatility remains a possibility as policymakers react to new data and evolving global dynamics.

From a technical perspective, regional market indices—including Germany’s DAX—are trading above key moving averages, with the DAX targeting new resistance levels and maintaining its trend channel established since August. Traders are closely watching to see whether this uptrend will persist or face a reversal as the quarter progresses.

In summary, European markets started the fourth quarter on a resilient note, carried by an outsized healthcare rally, stable macroeconomic data, and selective strength in key national markets. Yet, clouds remain on the horizon in the form of transatlantic political risks and an uncertain central bank outlook. As always, diversification and vigilance will be crucial for investors navigating this evolving landscape.

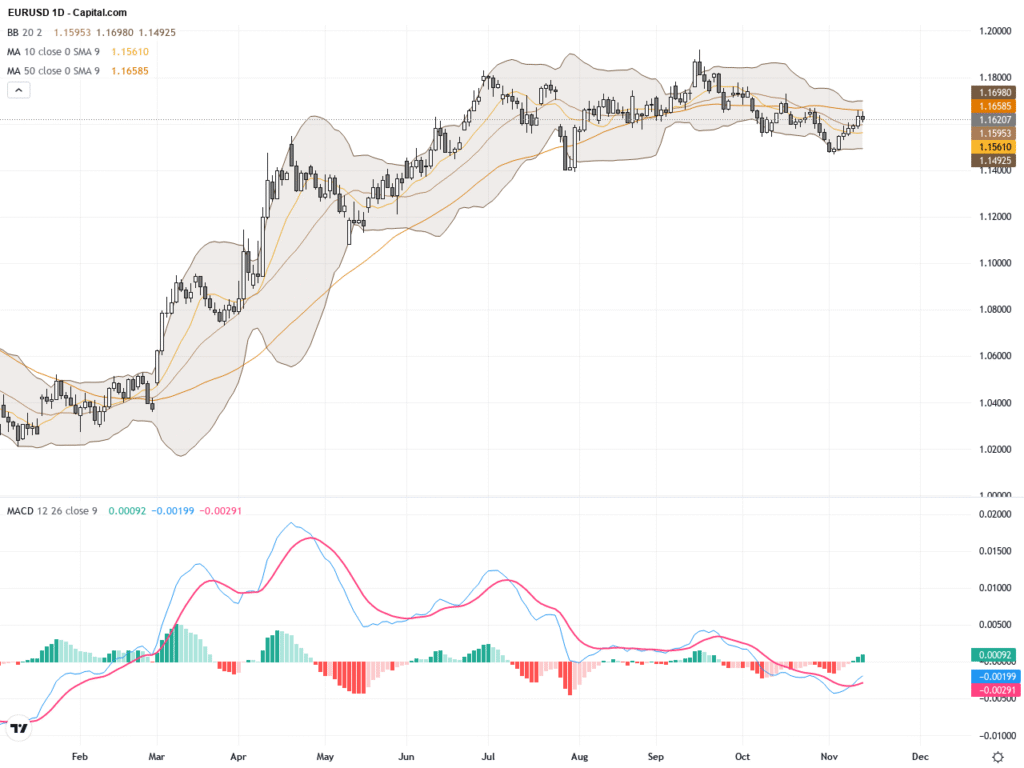

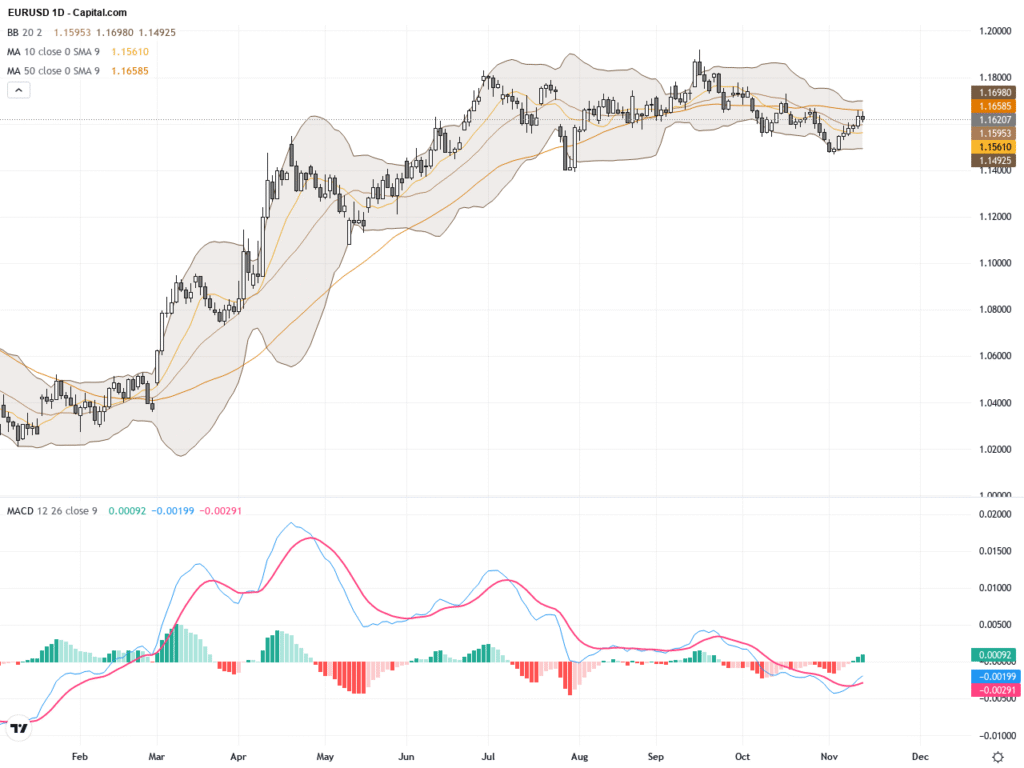

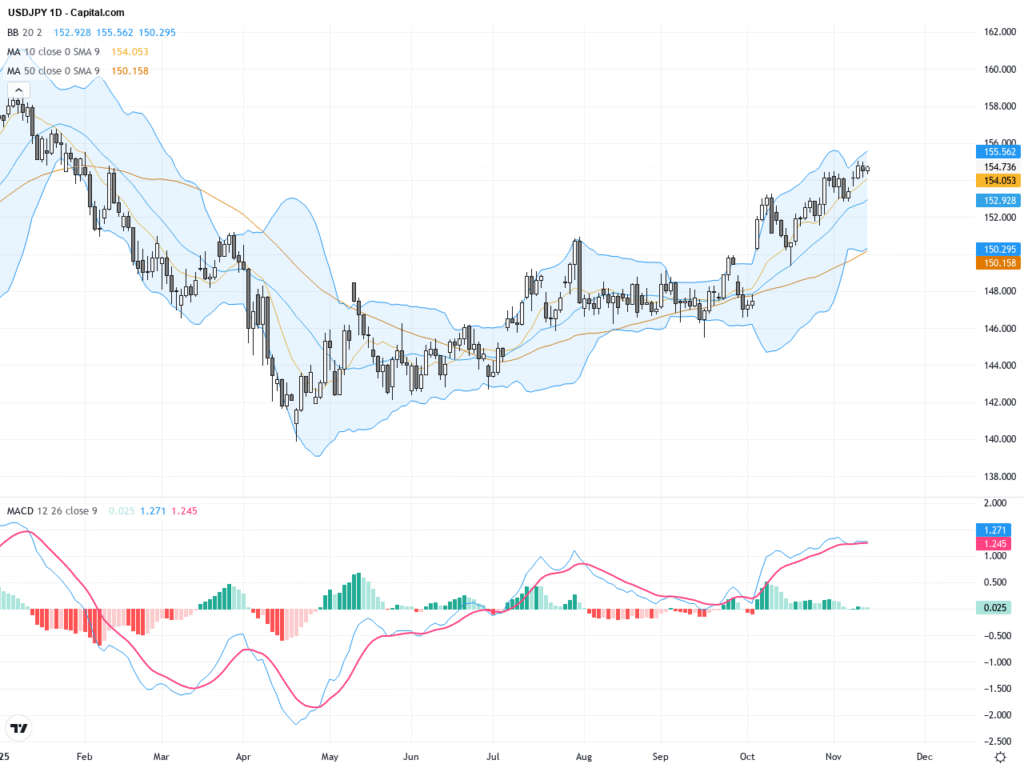

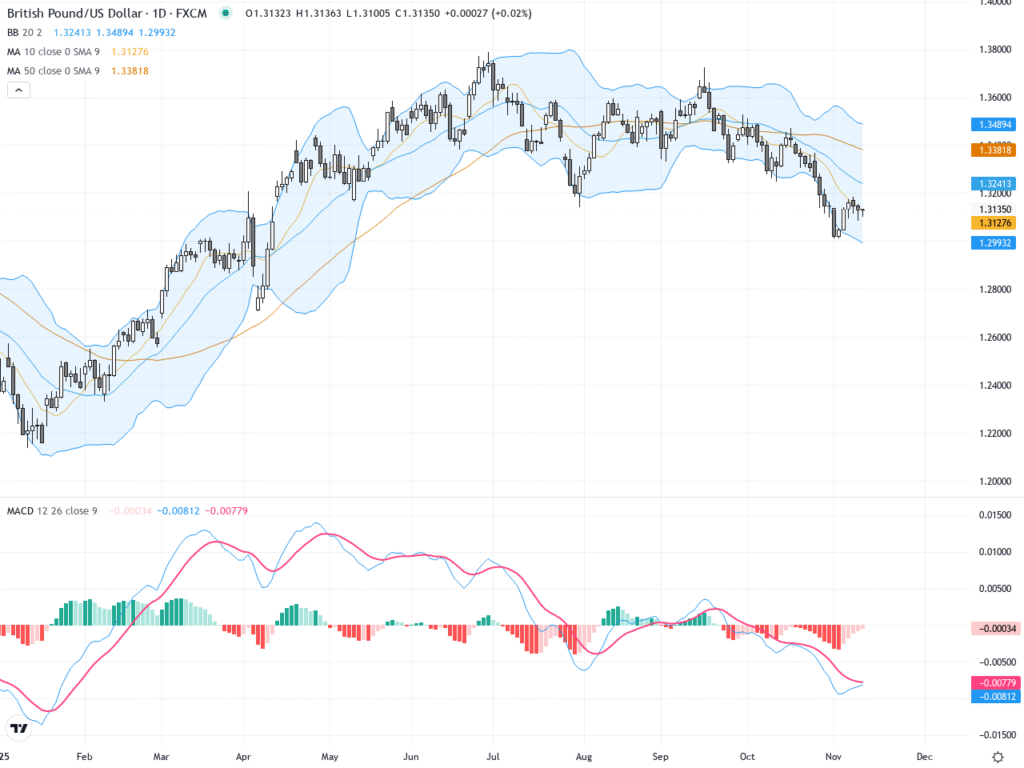

Latest Technical Analysis