|

| Gold V.1.3.1 signal Telegram Channel (English) |

Iran-Middle East Conflict Deepens Eurozone Slowdown as Energy Price Risks Surge

2026-05-22 @ 13:03

Iran-Centered Middle East Conflict Throws Cold Water on Eurozone Economy and Inflation Outlook

Over the past two months, the Eurozone’s economic pulse has weakened noticeably. May’s flash Purchasing Managers’ Index (PMI) data reveals that business activity in the private sector contracted for a second consecutive month, with readings dropping further below the key 50 mark that separates growth from contraction. Services sectors are bearing the brunt, while manufacturing is only mildly buoyant, but overall the trend points to a broad-based slowdown. This setback arrives just as the bloc was tentatively emerging from a mild technical recession, raising fresh concerns about stagflation-like pressures building up.

At the heart of this disruption is the escalating conflict centered on Iran and its wider Middle East neighborhood. The turmoil has sent energy and transportation costs soaring by disrupting supply chains and trade routes. Elevated oil and gas prices, combined with skyrocketing insurance and freight fees due to forced rerouting, have hit energy-intensive industries hardest. This input cost inflation threatens to unravel recent disinflation trends, making the European Central Bank’s task of balancing growth support and price stability even more delicate.

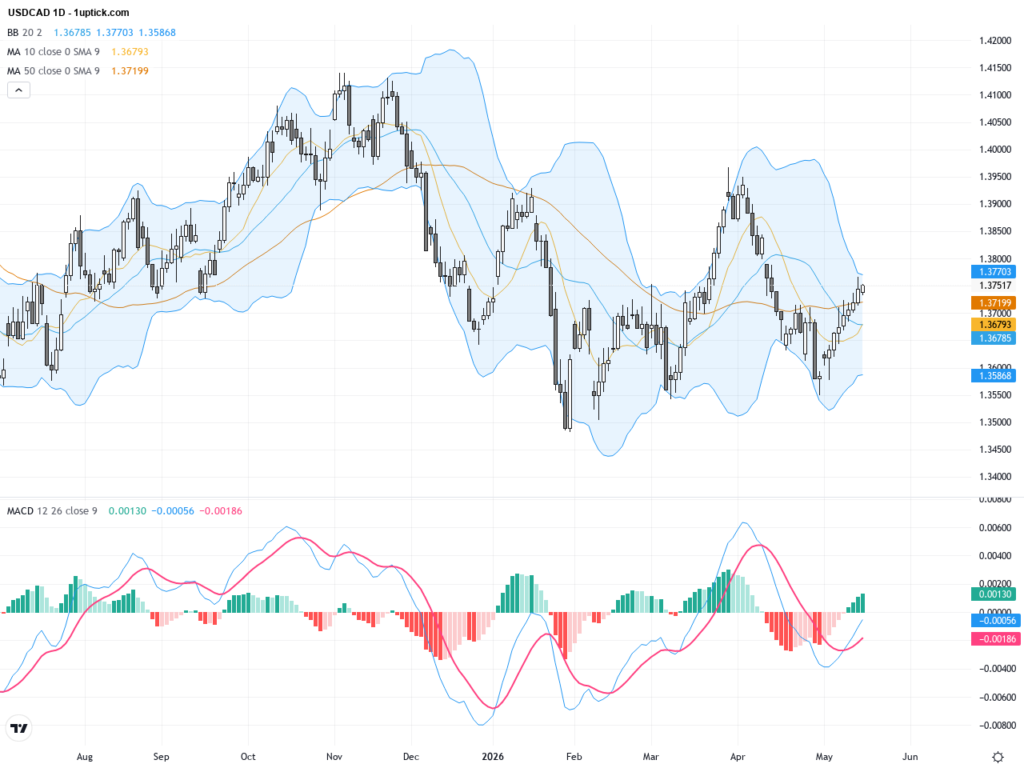

Currency markets tell a similar story: the euro has come under sustained downward pressure against the US dollar. Weak Eurozone economic data contrasts with relatively resilient US metrics, pushing investors to anticipate that the ECB will ease policy sooner than the Federal Reserve. Meanwhile, bond markets see a modest widening in peripheral Eurozone sovereign spreads versus German Bunds, signaling greater concerns about growth prospects and fiscal resilience amid the shadow of a protracted energy price shock.

Equity markets reflect this division. Energy and utilities shares have benefited from rising oil and gas price expectations, while consumer discretionary, industrials, and transport sectors lag behind due to squeezed household purchasing power and rising production and logistics costs. Corporate earnings forecasts increasingly cite geopolitical risk, rerouted shipping, and volatile energy supplies as key hurdles for the second half of the year.

Zooming into recent data, May’s PMI deterioration brings output to the weakest level in roughly two and a half years. Should these conditions persist, Q2 GDP growth could stagnate or dip negative. Key economies Germany and France both showed contraction, with France experiencing its steepest activity decline in over five years. Respondents to surveys highlight that war-induced energy and transport hikes, coupled with weaker external demand from conflict-affected regions, are dampening new orders and business confidence.

Looking ahead, energy prices remain critical to watch, especially as any escalation involving the Middle East’s supply infrastructure or shipping lanes could exacerbate market volatility. The ECB’s forthcoming policy meetings are likewise pivotal—how they navigate softening growth signals against renewed cost pressures will shape their interest rate trajectory. Markets broadly anticipate an initial ECB rate cut around mid-year, though the scope and speed of easing remain uncertain.

Further pressure points include the energy-intensive industries like chemicals, metals, transport, and manufacturing, which face margin squeezes from sustained high input prices. Consumer-facing sectors also risk softer demand amid rising living costs. If geopolitical tensions intensify or spread, the risk of a deeper Eurozone slowdown or recession will grow.

In short, the Iran-related Middle East conflict is no longer just a geopolitical flashpoint; it’s injecting fresh volatility into global energy markets and trade routes with direct knock-on effects for one of the world’s largest economic blocs. Investors and policymakers alike need to watch these evolving risks closely as the Eurozone grapples with a challenging and uncertain road ahead.