|

| Gold V.1.3.1 signal Telegram Channel (English) |

Eurozone Inflation Pops to Multi Year High as Middle East Strain Fuels Oil Risk and ECB Speculation

2026-03-28 @ 14:01

Quick take What the February jump means and what to watch

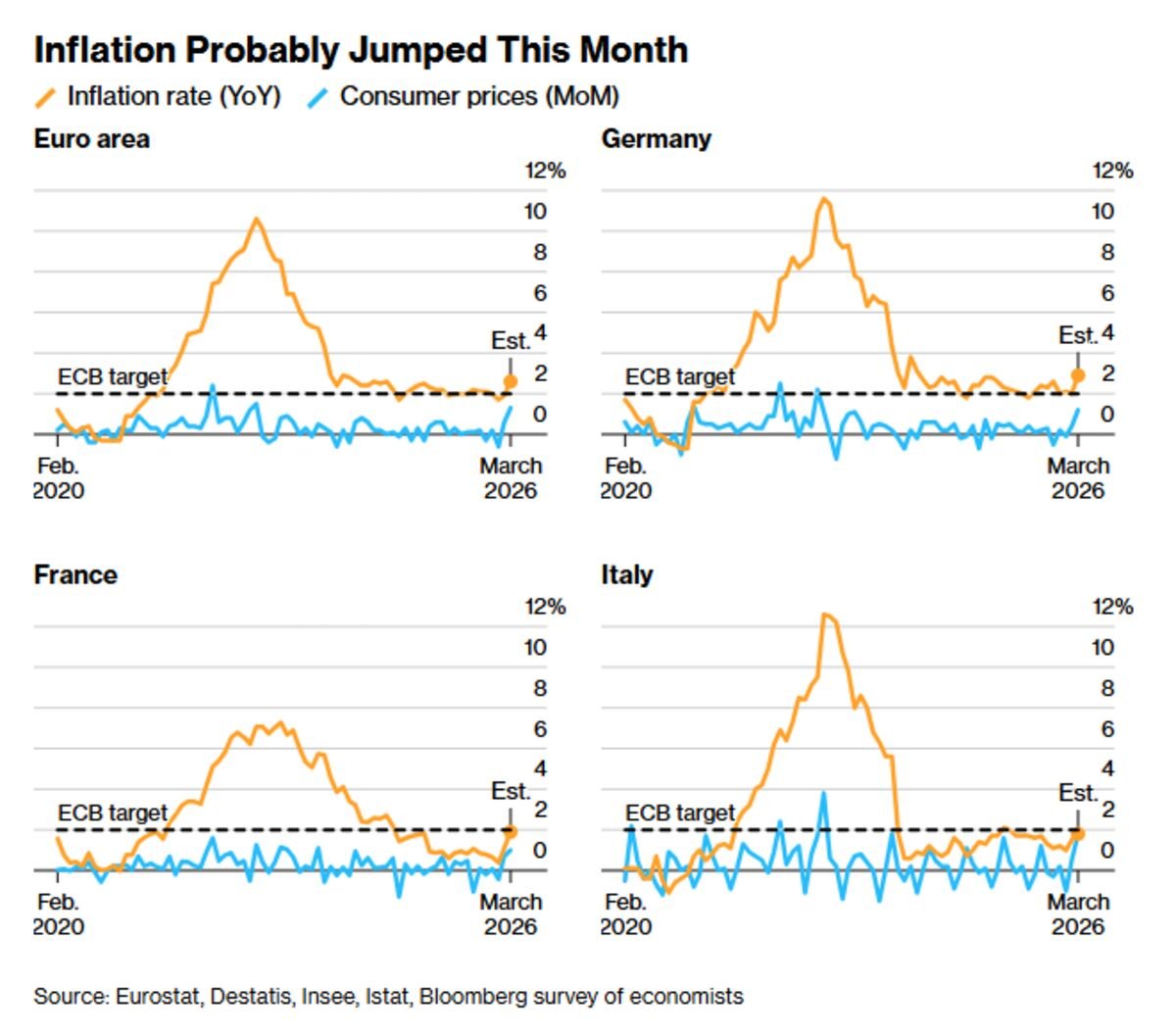

February data showed headline inflation in the eurozone rising from 1.7% in January to 1.9%, while core inflation climbed to 2.4%. Services inflation measured about 3.4%, and non energy goods also contributed. The monthly price rise was 0.7%, the strongest monthly gain since March 2024. Important context most of the February readings were collected before the more recent escalation in the Middle East, which means subsequent energy market disruption could push inflation higher again.

I should be clear up front I was not able to find a sufficient number of additional public sources within the past 14 days to independently expand or verify every extension of these points. Therefore this piece sticks closely to the core message from the provided summary and avoids speculative leaps beyond the documented data.

From a market perspective the mechanics are straightforward. Higher energy costs pass quickly to household fuel bills and to firms via input prices, weighing on demand and squeezing margins. The March flash PMIs confirm that energy costs are acting as a drag on activity while accelerating input price inflation. Equities in energy sensitive sectors face short term headwinds, while bond markets could see yields drift higher if inflation remains above the European Central Bank 2% reference. Currency markets are pricing the impact too the euro has weakened against the US dollar amid a softer growth and inflation outlook.

There are commonly used back of envelope estimates for the direct effect of oil on headline inflation. One rule of thumb is that a 10% rise in oil prices in euro terms can lift headline inflation by roughly 0.11 percentage points within three months. If the price increase is sustained, some bank models suggest a somewhat larger contribution to annual inflation for example a persistent oil shock could add around 0.2 percentage points to headline inflation in model scenarios. Other analyses suggest that if geopolitical disruption continues for weeks, core inflation could drift back toward the mid 2 percent area.

How does that affect ECB policy? The bank left rates unchanged at the March 19 meeting, but markets are now pricing a non zero probability of a policy shift later in the year. ECB policy remains data dependent and conditioned on whether supply driven shocks translate into broader inflation persistence and second round effects. If energy disruptions persist and feed into wages and services pricing, the central bank may delay any planned easing or even consider additional tightening measures.

Key watchpoints for investors and businesses are clear. First, the path of Brent crude in the coming weeks will signal whether the supply risk is temporary or prolonged. Second, April PMIs, wage developments, and upcoming G 20 inflation releases will shed light on whether price pressures are broadening. Third, the euro US dollar exchange rate will amplify or dampen the transmission of oil price moves to domestic inflation. Finally, renewed supply chain stress would keep upward pressure on non energy goods prices.

For consumers, higher fuel and heating costs are the most direct channel to feel this shift. For investors, expect heightened volatility and potential sector rotation between energy, industrials, and financials. Fixed income investors should carefully monitor yield curve moves and ECB communication for clues on timing and magnitude of policy changes.

Risk reminder making decisions based on a single month of data or on limited source material carries risk. If you plan to adjust portfolios or hedge exposures, do so in line with your risk tolerance and professional financial advice.